New Research: Revealing the consumer experience of digital finance in low- and middle-income countries

Digitalisation has transformed how we access our finance and the way we interact with those providing the services. In a post-Covid world, 57% of adults in developing economies now make or receive digital payments (an increase of 23% from 2014) and two-thirds of adults worldwide use digital payments. For people’s everyday lives, this means quicker transactions, improved access to essential products, and reduced travel time to withdraw and pay in cash. But in a relatively novel sector, consumers face a number of frustrations which impact their experience of digital financial services – such as system glitches, inappropriate design, fraud, cybercrime, data breaches, opaque pricing, and more.

The sector has a long way to go before our consumer vision of inclusive, safe, data protected and private, and sustainable services is realised. For this to happen, the consumer voice must be heard.

Our latest report - Digital finance: The consumer experience, 2023 - provides an assessment of the scale of the issue across low- and middle-income countries. In evaluating the pain points facing consumers, it provides a much-needed route map for regulators, consumer associations, and market actors to take action. Assessed across four ‘pillars’ of financial consumer protection, the total index score comes in at just 40 out of 100. These results make it clear that more work is needed to build consumer protection frameworks that sufficiently protect and empower consumers.

The report will be published in French and Spanish shortly.

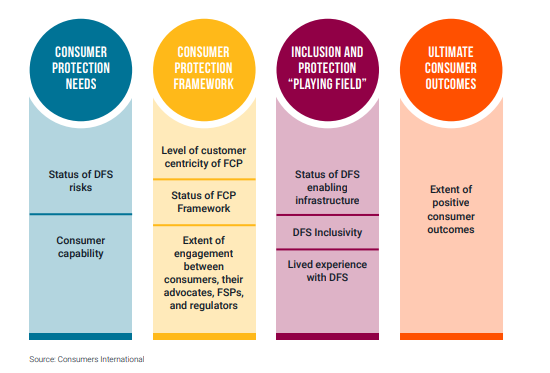

The four pillars are:

- Need for a financial consumer protection framework in the first place, centred on understanding the risks that consumers face and their ability to protect themselves against risk – such as by knowing their rights and responsibilities.

- Regulatory frameworks in place, whether based on consumer-centric principles and how they have sought participation from consumer representatives.

- How is financial service usage playing out for consumers? Do consumers actively use and have positive experiences with digital finance?

- Outcomes in real-terms for consumers. Are digital financial services making a difference to consumers’ financial health? What impact are they having on advancing sustainability?

What are the key takeaways?

- Action is needed to address how consumers experience the financial sector. Risk perception received an average score of just 27, and consumer capability to protect against risk just 36, showing a nervousness about engaging with digital financial services. Consumers also experience user frustrations, notably around safety, data protection and digital literacy. Together, these findings point towards a digital finance market which is failing to adequately or meaningfully protect consumers.

- More people than ever are using digital financial services, with access driven by improved internet access and widespread smartphone penetration. This was reflected in high scores in the enabling infrastructure and inclusivity elements, which received 54 and 65 out of 100 respectively. However, improving the quality and affordability of digital financial services remains a significant hurdle for the sector to overcome.

- The results for the outcomes pillar hold a disconcerting mirror up to the financial community – whilst there have been advances in financial consumer protection frameworks and financial inclusion – these have not yet translated into improved financial health and sustainability outcomes for consumers.

- Consumers are rarely present in financial sector regulatory decision-making processes, and their experiences are often left out of reported metrics on consumer protection. Financial consumer protection frameworks must go further and give consumers a real seat at the table.

What differences can be seen between economies?

Developing this tool has allowed us to take an interesting look at how different countries compare. Countries were categorised into three tiers, ‘advanced’, ‘transitioner’ and ‘emerging’.

Advanced and transitioner countries perform better due to having stronger protection frameworks and established independent recourse mechanisms and complaints systems in place. Meanwhile, ’emerging’ countries are lagging significantly behind in building strong financial consumer protection frameworks. Interestingly, the results showed limited variation between clusters on the inclusion and protection playing field pillar – which saw relatively high scores across all three tiers. This could be explained by the uptake of mobile money across low- and middle-income countries. In the years to come, annual instalments of this report will gather more data on remaining user frustrations allowing us to make deeper assertions on variation across countries.

What’s next?

Right now, we need a concerted effort to build consumer-level and system-level resilience to risk. The report lays out a call to action for decision-makers at the global and national level:

- Consumer associations should find innovative ways to engage with and educate consumers and proactively work with regulators to bring the consumer perspective into policymaking and regulation.

- Regulators should fill gaps in existing consumer protection frameworks to address the risks consumers are most worried about, and ensure that consumers are given a real seat at the table in the policy-making process.

- Financial service providers should build in consumer protection, empowerment and inclusion from the outset. This means using plain and transparent language, providing clear channels for recourse, and designing products and services that can effectively reach and empower marginalised consumers to engage in the financial sector.

- At all levels, actors should initiate action on bringing sustainability to digital financial services.

Consumers International will build these findings into the work of our Fair Digital Finance Accelerator – equipping market actors and others to heed our call to action and to ensure that consumer associations are actively involved. Over the next year we will also bring sustainability issues firmly to the digital finance agenda, exploring the massive opportunity for reaching climate goals and demystifying what sustainability in digital finance means in practice.

Useful links:

- Learn more about the Fair Digital Finance Accelerator

- Read our consumer vision for fair finance

- Find out how we are driving systemic change at the Davos Annual Meeting 2023

- Connect with us on Twitter, Facebook, LinkedIn and Instagram

- Contact us to collaborate as we explore opportunities for further research in this space