Resilience by Design: Building a new future for Digital Finance

A card tap. A keyboard click. A mobile phone interaction. Today’s digital payments, money transfers, loans and other financial services can often be accessed and transacted in seconds. But the lightning-fast evolution of digital networks and processes many of us rely on is creating an increasingly uneven playing field.

The fact that global access to digital financial services is expanding is a step in the right direction. Findings from the 2025 Global Findex Database report show 61% of adults – or 82% of account holders – in developing economies made or received a digital payment in 2024, up 27% from 2014.

However, bolstering access to digital services and systems without building-in protections leaves millions of consumers exposed to potentially confusing, unsafe, unfair or unethical practices, especially in low- and middle-income countries.

Findex defines resilient individuals broadly: as those who say they can come up with emergency funds within 30 days without much difficulty. Yet report findings show more than half of those surveyed in low-income countries state they could not meet the 30-day threshold.

A Consumers International survey of more than 3,000 people in eight countries shows as many as 75% of global consumers could be considered vulnerable to some extent. This goes beyond individuals exposed to sudden shocks like health costs or income loss, to include those with recurring conditions, like physical disabilities, or people with contextual factors, such as caring responsibilities, informal employment or low numeracy or digital capability.

To address this situation, we need a rethink. Design attitudes must begin to look forward in anticipation of users’ needs, instead of reacting to risks when they arise. Only then can we achieve inclusive, resilient and secure digital financial services for all.

Time for Action

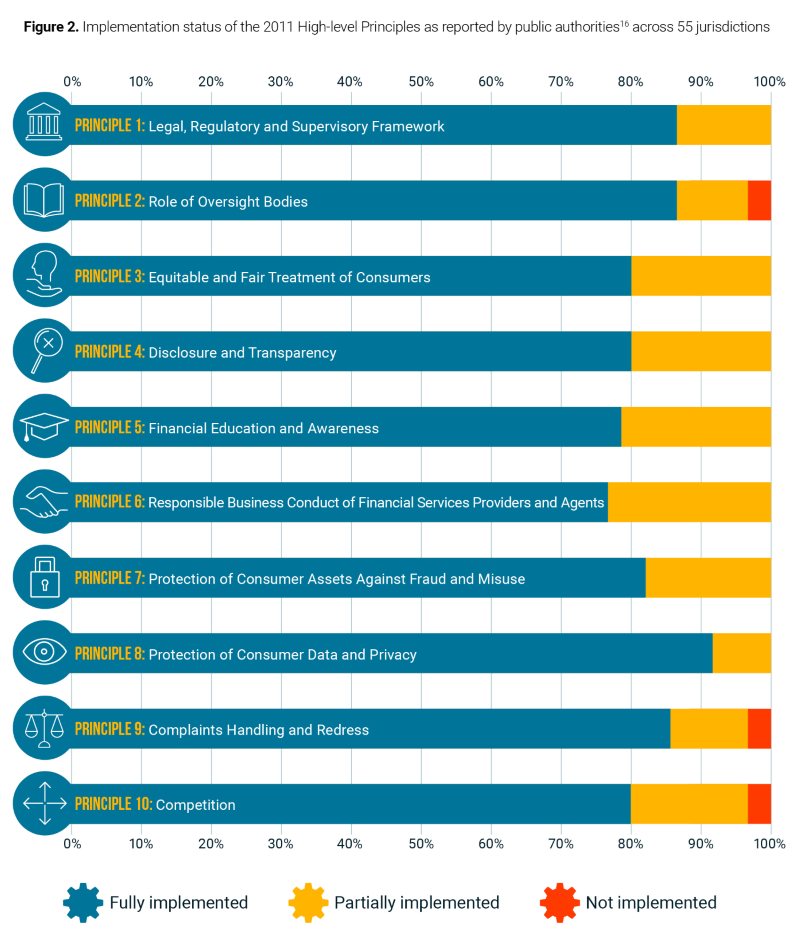

Today’s systems are designed to ensure financial services providers comply with rules guiding product design, disclosure, transparency and recourse. In 2011, the G20/OECD High-Level Principles on Financial Protection framework brought together ten principles of financial consumer protection. According to a 2021 OECD survey, most financial regulatory authorities have fully implemented all core principles.

Despite this progress, what’s written in law is not translating to positive change to people’s everyday lives. When consumers in the same countries are asked about their confidence in meeting basic needs, such as emergency medical costs, monthly bills, saving for retirement, or school fees, only around 30% say they are not worried at all.

In other words, regulation is a critical starting point, but it is one part of a much-needed effort to focus on genuine consumer outcomes.

Embracing Change

It’s important to accept there is no quick-fix here. Identifying and addressing vulnerabilities must go beyond good intentions to give consumers an active voice in helping regulators, policymakers and service providers tailor system developments to achieve positive outcomes.

Consumers International advocates for a fundamental shift in policy, alongside measurement of risks and vulnerabilities, the need for innovation to provide the necessary tools and processes to tackle issues, and a central role for consumer advocates to voice user concerns and experiences.

In some parts of the world the seeds of this transition are already being planted. The G20’s Global Partnership for Financial Inclusion initiative issued its Policy Note on Financial Well-being in 2024, providing a preliminary roadmap for a wellbeing measurement framework.

Leading by Example

At the national level, policymakers and regulators in countries like Brazil, UK and Malaysia are implementing policy initiatives aimed at making digital financial systems more resilient.

Malaysia’s Fair Treatment of Financial Consumers (FTFC) policy sets out several principles for consumer protection in the country’s finance sector, with real-world examples showing good and bad practices to help guide implementation.

In 2024, policymakers updated the policy to include a new principle: vulnerability. Financial service providers must develop policies, procedures and controls that safeguard consumers in vulnerable circumstances and ensure fair treatment at each stage of the customer journey: from product development through to complaints handling and redress systems.

In South America, the Central Bank of Brazil (BCB) and the National Monetary Council (CMN) issued Joint Resolution 8 in 2023 to enhance financial education and wellbeing, particularly among low-income households.

Financial institutions must collaborate with consumer advocates to create user-friendly tools, educational content and internal policies to help users understand and manage their finances more effectively. Progress on financial education and wellbeing must be monitored using set targets and indicators, with data collected using metrics – like the percentage of consumers holding minimum savings equalling three months of expenses – to ensure continuous improvement.

Meanwhile in the United Kingdom (UK), industry regulator the Financial Conduct Authority introduced its Consumers Duty policy in 2022. This progressive policy directs financial services providers to set higher standards for consumer protection and deliver positive outcomes for all consumers, including those from vulnerable groups.

Rather than focussing solely on tick-box compliance, the policy encourages customer-centric design and innovation to promote positive customer outcomes across both traditional and digital digital financial business models. As with Brazil’s Resolution 8, monitoring and data-driven insights play an important role in identifying and addressing issues before they cause harm, while ensuring robust consumer protection, transparency and accountability.

These are just a few emerging approaches that reimagine the architecture of digital financial services systems, with more protection, inclusion and trust built into the design.

Better by Design

A seismic shift in attitudes is required to design digital finance systems that can help eliminate unsafe, unfair or unethical practices and ensure safe and sustainable goods and services for all.

To this end, Consumers International is developing a “guiding star” framework as part of a Building Consumer Resilience in Digital Finance report, to promote future action that prioritises the consumer voice.

This framework for action focuses on five key design elements: consumer voice; consumer wants and needs; representation and engagement; supervision; and consumer impact measurement.

For regulators, policymakers and financial services providers looking to build more resilient digital financial infrastructure and systems, the report outlines a path to adopt outcomes-based regulation, integrate real-time consumer risk monitoring and design Digital Public Infrastructure (DPI) with user protection built in.

It’s a way of uniting governments, service providers and consumer organisations toward a shared vision for inclusive, people-centred digital finance that anticipates and addresses user needs, wherever they are and whatever the circumstances. It’s a collective voice that needs to be heard.